As a restaurant operator, understanding the financial nuances of your operation is a crucial part of your ongoing success. Although some people may use the terms “recipe costing” and “food costing” interchangeably, they refer to very different processes with distinct roles in helping you control costs and analyze profitability.

When costing a dish, it’s essential to understand the differences between these two restaurant metrics and what they can tell you about your restaurant’s financial health.

Recipe Cost vs. Food Cost

Understanding the distinction between recipe costing and food costing allows operators to pinpoint expenses more accurately and make informed decisions that contribute to the business’s overall health.

Recipe costing focuses on calculating the cost associated with the ingredients in each dish, making it easier to determine proper pricing. Food costing provides a broader view of how food expenses impact the restaurant’s total revenue.

Both metrics are essential, but they serve different purposes and offer unique insights that, when combined, can provide a comprehensive picture of a restaurant’s financial performance.

What is Recipe Costing

Recipe costing is the process of calculating the total cost of all ingredients used to prepare a specific dish. This measurement includes every component, from primary ingredients, like meats and vegetables, to minor additions, like herbs and spices.

Breaking down these individual costs allows restaurant owners to establish a baseline price for each menu item. These baseline costs can then help ensure that the menu prices listed for each dish can be profitable, even when accounting for other operational expenses, such as labor or overhead.

Why Use Recipe Costing?

As a tool, recipe costing is primarily utilized to determine smart and effective pricing strategies. The level of granularity in calculating the individual ingredients within each recipe can help you gain a clear understanding of your margins, allowing you to make informed pricing decisions.

Key reasons for using recipe costing include:

- Setting profitable menu prices.

- Supporting menu engineering.

- Enabling theoretical food costing.

- Controlling portion sizes.

- Standardizing across locations.

What Is Food Costing?

Food costing is the process of calculating the overall cost of the food and ingredients used in a restaurant over a specific period. These calculations are not limited to individual dishes but encompass all food-related expenses during the evaluated timeframe.

This metric includes the cost of purchasing food items directly involved in cooking. However, it can also include the costs of spoiled or damaged items, paper products and other general-use goods, and portion control products.

Why Use Food Costing?

Calculating food cost provides a high-level view of your restaurant’s food control processes over time. It can help identify inefficiencies and reduce unnecessary spending, such as through excessive waste and inefficient portion sizes.

Key reasons for using food costing include:

- Measuring operational efficiency.

- Tracking trends over time.

- Informing inventory purchase decisions.

- Uncovering hidden losses.

- Guiding staff training.

Costing a Dish Using Recipe Costing

Recipe costing allows operators to dive deep into the specifics of ingredient costs, breaking them down to the minutest detail. This granular analysis can help set a profitable price point for each dish. It can also reveal where individual product costs are fluctuating and how the chosen ingredients contribute to the overall cost of making a dish.

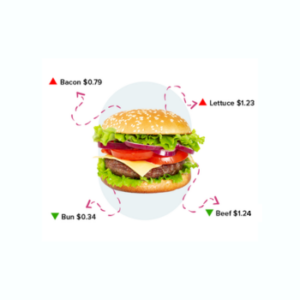

Once the price of each ingredient is determined, it’s converted into an associated portion cost for that dish. For example, the ground beef associated with making a burger may be calculated at $5.00 per pound and then converted to $0.31 per ounce ($5.00 / 16 ounces per pound) to calculate the total cost of the patty. In this example, a quarter-pound (or 4-ounce) patty would translate to a portion cost of $1.24. Once each portion cost is calculated, they’re added together for a total dish cost, which operators can use to set a profitable menu price.

Costing a Dish Using Food Costing

Food costing can give managers a much broader view of food-related expenses by analyzing costs as they’re incurred across a specific period. Unlike recipe costing, which zeroes in on the costs associated with an individual menu item, food costing is calculated as the total cost of goods sold (COGS) during the period. To get the best picture of costs and how they influence profitability within the restaurant, most operators analyze food costs on both a theoretical and actual basis.

Analyzing Theoretical Food Cost

Theoretical food cost is calculated based on the assumption that every ingredient is used precisely according to the recipe without any waste, spoilage, or over-portioning. Operators calculate the number of dishes sold during a given timeframe, then use the recipe cost of those dishes to calculate what the food cost theoretically should be in a perfect world. By starting with this value, operators can clearly identify how much additional food cost can be attributed to outside factors.

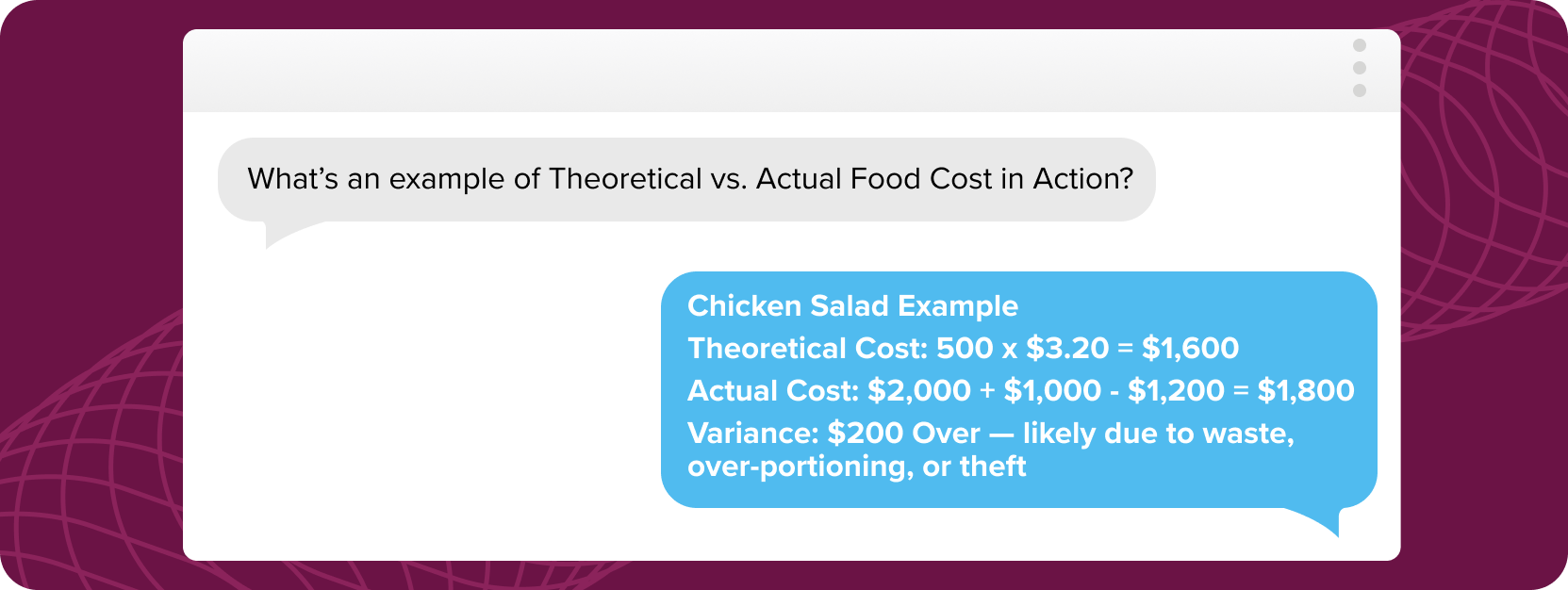

Theoretical Food Cost Example

Let’s say a restaurant sells 500 chicken salads during the month. The recipe cost for all the ingredients in one salad is $3.20. In this scenario, the theoretical food cost for the month would be:

500 salads x $3.20 = $1,600

This is the amount the restaurant would expect to spend on ingredients if each salad were perfectly portioned and there was no waste.

Analyzing Actual Food Cost

Actual food cost is calculated by analyzing the real-world expenses incurred by a restaurant to produce its dishes over a specific period. Operators use beginning and ending inventory numbers for the period, along with inventory purchases during that period, to determine how much inventory was actually used during that period. Calculating both theoretical and actual food cost numbers and comparing the two can help operators identify inefficiencies and opportunities for better cost control.

Actual Food Cost Example

Continuing with the chicken salad example, let’s say the beginning inventory of salad ingredients (chicken, romaine, croutons, and dressing) was valued at $2,000. They purchased an additional $1,000 worth of the salad items during the month and counted the ending inventory for these items to be $1,200. In this scenario, the actual food cost for the month would be:

$2,000 beginning inventory + $1,000 purchases – $1,200 ending inventory = $1,800

While the theoretical food cost for the chicken salads was $1,600, the actual food cost usage was $1,800, indicating a $200 variance (likely due to over-portioning, waste, or theft).

Best Practices for Controlling Food Costs

Both recipe costing and food costing have their place in helping restaurant owners and managers control operational costs. Understanding the difference between these two restaurant metrics and how to use them effectively is the first step in maintaining effective cost control strategies. Operators can also leverage these additional best practices for an even more comprehensive approach to operational cost management.

Menu Pricing and Optimization

Menu pricing is one of the most direct ways a restaurant can influence its food cost percentage and overall profitability. By continuously monitoring and adjusting menu prices and exploring ways to optimize menu offerings based on cost data and sales trends, restaurant owners can maintain a balanced approach to controlling margins. By understanding the true cost of each dish and setting realistic cost targets, operators can design a menu that supports both customer satisfaction and financial performance.

To use menu pricing as a cost control tool, review your menu items regularly. High-volume items with low profit margins may be dragging down your overall performance, while lower-selling but high-margin items might benefit from stronger promotional efforts. Menu optimization also includes evaluating the structure of the menu itself to highlight high-margin and best-selling items to maximize sales.

When done effectively, menu pricing and optimization serve as a continuous feedback loop where recipe-level cost data and food cost analysis inform pricing and menu decisions, which in turn influence purchasing and operational behavior. This approach can help keep costs under control and maintain a healthy balance with guest value and satisfaction, ultimately strengthening your bottom line.

Budget Planning and Forecasting

Routinely setting aside time for budgeting and forecasting can help operators create a financial roadmap to guide operational decision-making and resource allocation. Without this roadmap, managers are steering their restaurant without a compass and making decisions about all the major cost contributors reactively rather than proactively.

Utilizing data from both recipe costing and food costing is crucial in the budgeting and forecasting process. The detailed insights garnered from recipe costing—such as the cost of individual menu items—enable operators to set menu prices that will help maintain a balanced and profitable budget. Food costing provides a holistic view of overall food expenses, allowing operators to better predict future costs and plan them into a budget accordingly.

By integrating these two data sets, restaurant managers can make more accurate projections about future costs and revenues, ultimately leading to leaner operations and more consistent profitability.

Variance Analysis and Inventory Management

Variance analysis involves comparing theoretical food costs, based on standard recipes and portion sizes, with the actual food costs recorded. This process can help identify discrepancies, such as waste or over-portioning, so managers can quickly determine where to focus their efforts in managing operational issues. Managers should also implement strong inventory management strategies to maintain optimal stock levels, which can help minimize waste and prevent stock-outs.

Recipe costing and food costing work together in these variance and inventory processes to give operators the specific data needed to facilitate better inventory purchasing decisions and more accurate variance analysis.

Frequently Asked Questions

How is recipe costing different from food costing?

The key difference between food costing and recipe costing is the scope they cover. While recipe costing isolates the cost of ingredients for a particular dish, food costing examines the aggregate food expenses during a specific operating period to manage and streamline the restaurant’s overall food expenditure.

Together, these two cost metrics provide a rounded perspective on how food costs impact profitability, enabling more informed decision-making in pricing, budgeting, and operational practices.

When costing a dish, is it better to use the recipe costing method or the food costing method?

The recipe costing method is generally more effective for costing an individual dish, as it allows you to break down the cost at the ingredient level for each menu item. By contrast, the food costing method is typically more effective for costing all of the dishes within a restaurant’s menu. Food costing allows you to look at all food expenses in aggregate and make macro-level decisions about inventory and food cost management.

Is costing a dish really worth the time and effort?

Costing a dish is worth the time and effort required because it can help operators make informed decisions about pricing strategy and operations. These decisions directly impact your restaurant’s profitability, so any effort spent on these processes can translate to significant improvements in your bottom line. Fortunately, operators can greatly reduce the time and effort required to calculate the cost of each dish by leveraging automated technology tools, such as Back Office.

How can I save time and still manage food costs in my restaurant?

Leveraging technology tools available through Back Office can significantly streamline food cost management processes, saving valuable time and improving your calculations’ accuracy. Tools such as automatic recipe costing calculators, real-time inventory tracking, and detailed variance analysis reports can help simplify many labor-intensive tasks in managing food costs. By automating these critical processes, restaurant managers can focus more on delivering exceptional dining experiences and less on manual cost management processes.

Costing a Dish Using Automation

While both recipe costing and food costing might seem like separate processes that take up more of your valuable time, a deeper understanding of how these restaurant metrics work together can help you leverage efficiencies and improve profitability within your restaurant. Recipe costing provides the granular analysis necessary to help you set individual pricing levels, while food costing provides the broader perspective needed for comprehensive budgeting and strategic operational decision-making.

Utilizing a technology-based solution such as Back Office can help you integrate both approaches seamlessly and achieve a balanced and efficient cost control system, ultimately driving profitability and ensuring operational success.